Jeremy Green is the Head of UK Team at Agreus Group. With more than 15 years experience as a broker and another decade spent as a Director and Managing Consultant in the Recruitment Sector, he comments on Investment Compensation and how our Bonus Benchmark Report highlights a change in the way Family Offices invest.

Read Jeremy's take on Executive Investment Compensation below and scroll to receive your free copy of the report.

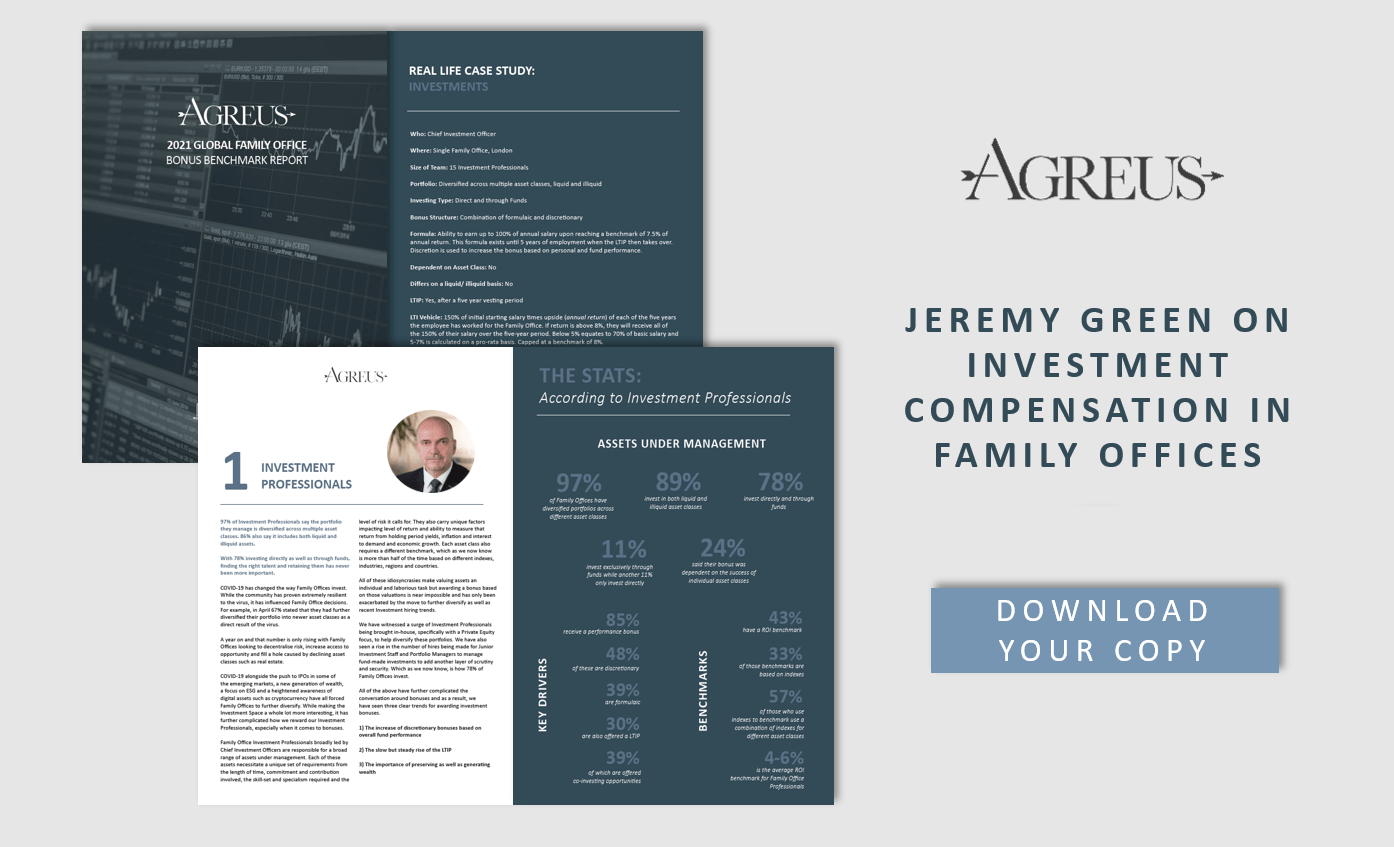

97% of Investment Professionals say the portfolio they manage is diversified across multiple asset classes. 86% also say it includes both liquid and illiquid assets.

With 78% investing directly as well as through funds, finding the right talent and retaining them has never been more important.

COVID-19 has changed the way Family Offices invest. While the community has proven extremely resilient to the virus, it has influenced Family Office decisions. For example, in April 67% stated that they had further diversified their portfolio into newer asset classes as a direct result of the virus.

A year on and that number is only rising with Family Offices looking to decentralise risk, increase access to opportunity and fill a hole caused by declining asset classes such as real estate.

COVID-19 alongside the push to IPOs in some of the emerging markets, a new generation of wealth, a focus on ESG and a heightened awareness of digital assets such as cryptocurrency have all forced Family Offices to further diversify. While making the Investment Space a whole lot more interesting, it has further complicated how we reward our Investment Professionals, especially when it comes to bonuses.

Family Office Investment Professionals broadly led by Chief Investment Officers are responsible for a broad range of assets under management. Each of these assets necessitate a unique set of requirements from the length of time, commitment and contribution involved, the skill-set and specialism required and the level of risk it calls for. They also carry unique factors impacting level of return and ability to measure that return from holding period yields, inflation and interest to demand and economic growth.

Each asset class also requires a different benchmark, which as we now know is more than half of the time based on different indexes, industries, regions and countries.

All of these idiosyncrasies make valuing assets an individual and laborious task but awarding a bonus based on those valuations is near impossible and has only been exacerbated by the move to further diversify as well as recent Investment hiring trends.

We have witnessed a surge of Investment Professionals being brought in-house, specifically with a Private Equity focus, to help diversify these portfolios. We have also seen a rise in the number of hires being made for Junior Investment Staff and Portfolio Managers to manage fund-made investments to add another layer of scrutiny and security. Which as we now know, is how 78% of Family Offices invest.

All of the above have further complicated the conversation around bonuses and as a result, we have seen three clear trends for awarding investment bonuses:

1) The increase of discretionary bonuses based on overall fund performance

2) The slow but steady rise of the LTIP

3) The importance of preserving as well as generating wealth

Read our Bonus Benchmark Report to see how yours or your staff bonuses compare.